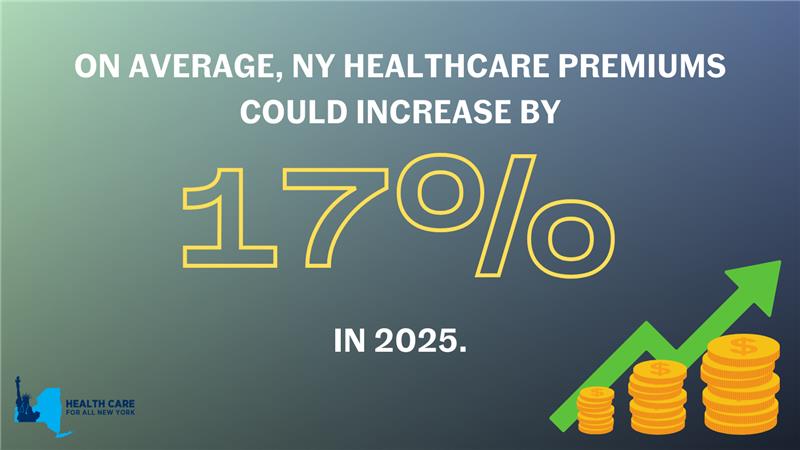

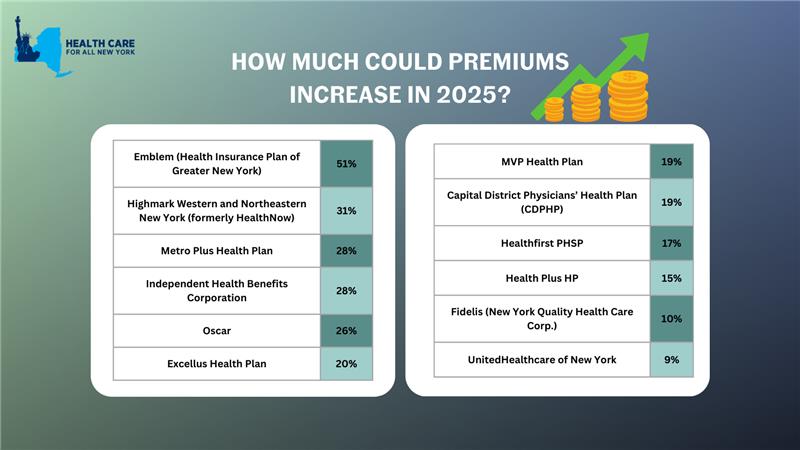

New York’s individual market premiums might increase by up to 17 percent in 2025. New York’s twelve individual market carriers are requesting increases ranging from 9 percent by MVP to a shocking 51 percent by Emblem. These requested increases far surpass requests from carriers in other states.

In our comments, HCFANY breaks down why DFS should curb each carrier’s specific rate requests to protect patients from another unaffordable increase in health care costs. Find your carrier in the list below to see what we had to say:

- CDPHP

- Emblem

- Excellus

- Fidelis

- Healthfirst

- HealthPlus

- Highmark

- Independent Health

- Metroplus

- MVP

- Oscar

- United

New York’s individual market insurance carriers plan to increase premiums by an average of 17% in 2025. This month, consumers have the opportunity to weigh in to make our voices heard. The State already approved premium increases of over 14% on average in 2024, another 17% would make health insurance out of reach for many New Yorkers.

Depending on your carrier, premiums could increase between 9% and 51% in 2025, impacting New Yorkers’ ability to spend on necessities such as health care, groceries, and transportation. It is critical that consumer voices are heard to prevent health insurance from being even more unaffordable.

Make your voice heard: submit a public comment before June 28, 2024 sharing how steep premium increases would impact you and your loved ones.

Tell the State how more expensive premiums would impact you by leaving a public comment here by Friday, June 28. Share a personal story on your healthcare needs and affordability concerns you have, or use the following sample for guidance:

“My plan, (insert carrier name), has asked for a (insert from table below) % premium increase. I already struggle to afford health insurance and that increase would require me to sacrifice ____.”

New York State of Health (NYSOH) has included several exciting new initiatives in its 2025 Plan Invitation. Though some of the initiatives are subject to federal approval, HCFANY is thrilled about the improvements to the quality and affordability of health insurance plans offered on the NYSOH marketplace. Here are some key wins for consumers:

- Eliminating in-network cost-sharing for New Yorkers with diabetes in State-regulated plans. The program applies to medical care, prescription drugs, supplies, and diagnostics related to the primary diagnosis of diabetes.

- Cost-sharing subsidies for low- and moderate-income New Yorkers on Qualified Health Plans (QHP) with incomes up to 400 percent of the Federal Poverty Level (FPL), or $125,000 for a family of four. If approved, NYSOH will use $315 million of federal waiver passthrough funding that was allocated for these subsidies in the 2024-25 State Budget.

- Expanding maternal health cost-sharing initiatives to QHPs to allow pregnant and post-partum New Yorkers to access zero copay care for almost all diagnoses and services through 12 months postpartum.

- Eliminating waiting periods for standalone dental plans offered through NYSOH for all adult dental services (exception for orthodontics), allowing New Yorkers to use the coverage they are paying for.

The New York State Department of Health (DOH) Maternal Mortality Review Board has released a new report, providing a detailed review of maternal deaths across the state between 2018 and 2020. Here are the findings:

Overall, the prevalence of maternal mortality in New York State remains below the national average; however, racial disparities in maternal outcomes unfortunately tell a different story. Nationally, Black mothers die at more than double the rate of White mothers. In New York, Black mothers die at five times the rate of White mothers. Black mothers in New York have a higher prevalence of maternal mortality than the national average.

The state recorded 121 pregnancy-related deaths between 2018 and 2020. The review found that almost 74% of these maternal deaths were preventable. In addition, discrimination was a likely contributing factor in almost half of maternal deaths.

It is imperative that the state continues to take action to eliminate preventable maternal deaths and improve outcomes for women of color, particularly Black women. HCFANY will continue to advocate for interventions to reduce racial disparities and overall mortality of birthing New Yorkers.