The season of giving is coming early for many New Yorkers seeking hospital care this year. As of last month, amendments to New York’s Hospital Financial Assistance Law (HFAL) will make it easier to apply for and cover more patients under financial assistance programs. The HFAL, also known as Manny’s Law, was implemented in 2006 in response to the death of Manny Lanza, 24. Lanza passed away after being denied life-saving surgery due to his uninsured status.

Financial assistance programs help many patients receive affordable care on a sliding fee scale based solely on their household income. This includes patients who are uninsured or those with insurance, but medical costs are a big strain on their income. Rising hospital prices in recent years have left many patients unable to afford the care they need, often leading them to incur medical debt. A 2023 Urban Institute reported that 740,000 New Yorkers had medical debt, with nearly half of them owing $500 or more. This updated HFAL will streamline the process and expand the eligibility of hospital financial assistance. New Yorkers will finally be able to have some more relief from medical debt and rising healthcare costs.

The following changes will be made to HFAL and medical debt in New York.

- All hospitals licensed by the New York State Department of Health (NYSDOH) are required to use a Uniform Hospital Financial Assistance form and inform patients of financial assistance availability in writing during registration and at discharge (regardless of the hospital’s participation in the Indigent Care Pool). Eligibility will not consider the patient’s immigration status. Before this amendment, many patients were never informed financial assistance existed and many hospitals requested information that was not legally required, like Social Security Numbers or tax returns, which often scared patients away from applying.

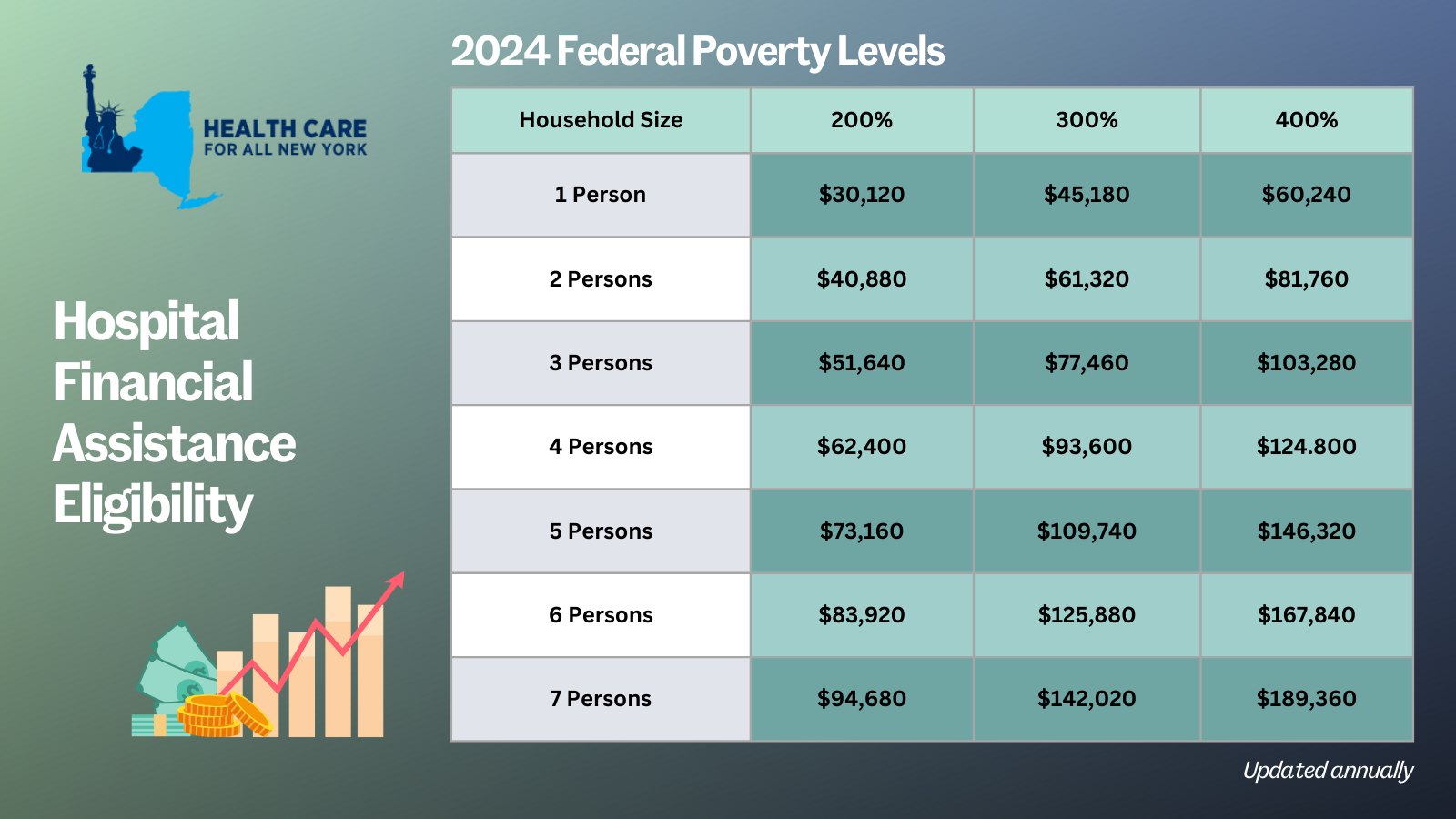

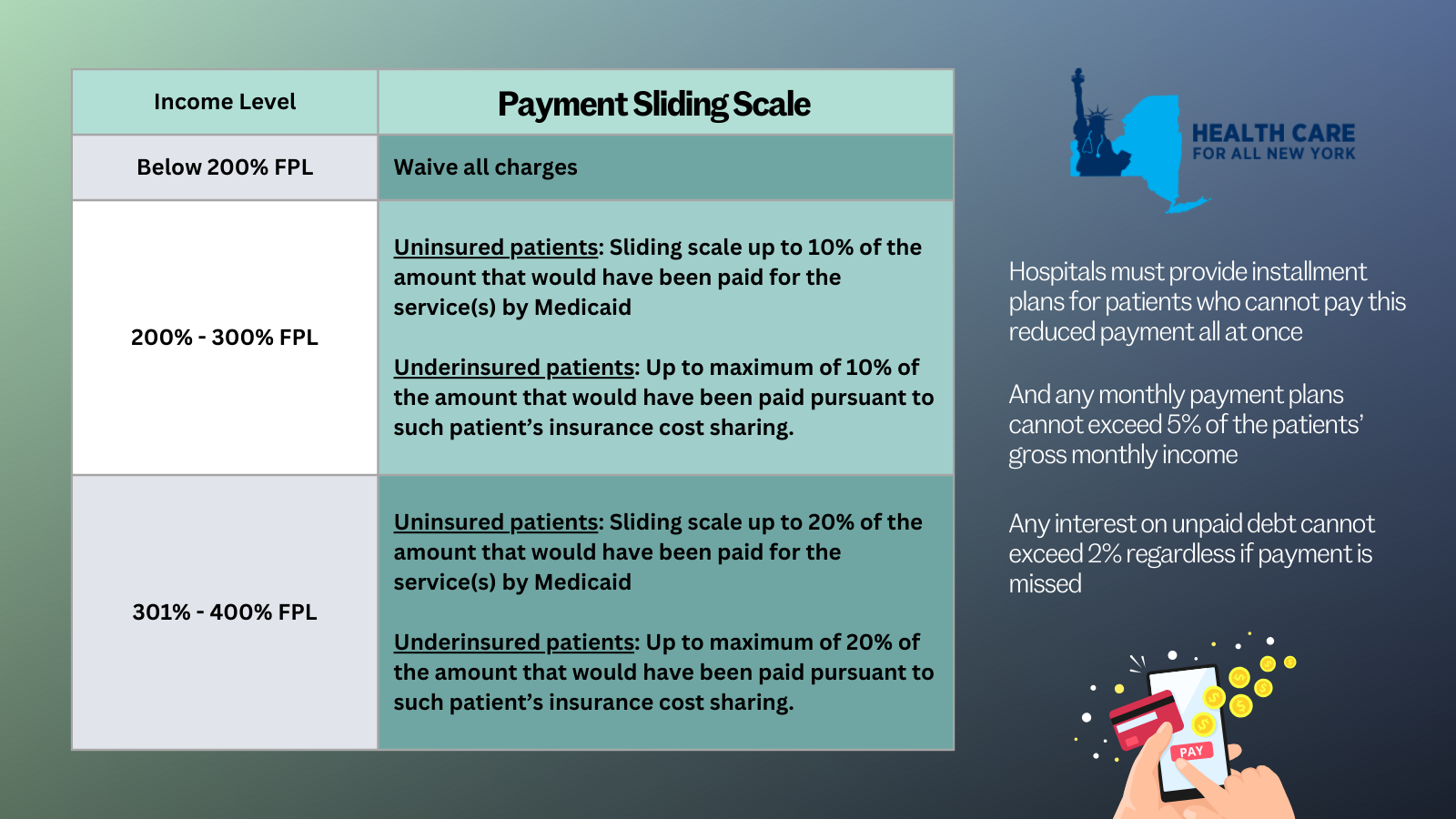

- Patient eligibility for financial assistance will be expanded for those uninsured and underinsured. Under the new law, being underinsured is defined as patients whose paid medical expenses, excluding insurance premiums, exceeds 10 percent of their income within the last 12 months. Uninsured patients will now qualify if their household earns up to 400 percent of the federal poverty level (FPL) and will receive free or discounted care based on a sliding scale (see the table below for eligibility guidelines based on household size and the payment sliding scale). These guidelines will be solely based on the FPL and are updated through the Poverty Guidelines | ASPE.

- Individuals can now apply for hospital financial assistance at any time.

- Hospitals may not sell patients’ debt to third party entities like debt collection agencies. Often these agencies use aggressive and threatening practices to make patients pay medical debt.

- Hospitals are prohibited from bringing lawsuits against patients earning up to 400 percent FPL to collect unpaid medical bills. And lawsuits to collect unpaid balances cannot be brought until 180 days after the first medical bill. Lawsuits have disproportionately affected people of color and low-income residents. For example, according to a 2024 Community Service Society of New York report, over a third of lawsuits filed by State-run hospitals were filed against patients who lived in zip codes where residents are disproportionately people of color. Additionally, nearly all these cases were filed against patients that should have been eligible for hospital financial assistance.

- To measure this impact, hospitals will report to the DOH the number of people that have applied for financial assistance annually including age, gender, race, ethnicity, and insurance status.

With this series of reforms, more New Yorkers will be able to receive affordable hospital care and reduce their chances of incurring medical debt. The HFAL was a landmark reform back in 2006 and has been far improved with these amendments.

Here’s a copy of the form hospitals must use now.

If you need assistance in applying for hospital financial assistance, contact Community Health Advocates at 888-614-5400.

The NY Senate just passed the Fair Medical Debt Reporting Act (S4907A/A6275A), an important step toward protecting patients from the long-term consequences of medical debt.

This bill would prohibit medical debt from being collected by a consumer reporting agency or included in a consumer report. Now we need your help urging the NY Assembly to follow the Senate’s lead and pass the Fair Medical Debt Reporting Act (S4907A/A6275A).

One patient who shared his story with us, David S., had his credit score slashed in half due to medical debt. This means he can no longer buy trucks for his towing business, his main source of income.

David’s story is only one of many. We can’t allow this to keep happening — New Yorkers deserve better. Please take action with us today to protect patients!

Nancy Rodriguez, a 66-year-old Queens resident, struggles with a number of life-altering cardiopulmonary medical conditions. She works at a doctor’s office despite her disability, to supplement her modest Social Security benefits.

Nancy’s total income is about $30,000 a year, including Social Security — too much to qualify for ordinary Medicaid. Since 2017, she has used the Medicaid Buy-in Program for New Yorkers with Disabilities (MBI-WPD) to cover her medications, multiple specialist visits, and hospitalizations.

Still, Nancy has spent years mired in medical debt. In 2020, her medical bills totaled $500,000, including a 13-day hospitalization for COVID. In 2022 she owed $300,000 for a couple of hospitalizations and a surgery.

“For me to be without health insurance is not acceptable, not even for five minutes.”

Under current law, the MBI-WPD program is limited by income, assets, and age. In her FY2024 Executive Budget, Governor Hochul has proposed expanding the program, so that more New Yorkers with disabilities can work and still qualify for Medicaid coverage.

The Governor has proposed removing the age limit of 65, which Nancy says, “would be a godsend for me.” She does have Medicare, but she does not know how she would manage a Medicare Part B premium, a supplemental “Medigap,” and a drug plan which she figures could amount to $300 per month. “I don’t have that kind of money and I work as many hours as I can. It’s very frightening. I lose a lot of sleep over this.“

We look forward to the passage of New York State’s budget including the expansion of Medicaid Buy-in coverage so that people like Nancy will not have to lose sleep over medical bills and can continue to work. Nancy says, “I am very fortunate that I am able to work and I will continue to work as long as I can do it.”

Let’s keep Nancy working and with critical health coverage.

Today, an extraordinarily diverse group of 61 organizations representing patients, religious leaders, labor organizations, people who are older, have disabilities, immigrants and people of color and more sent a letter to Majority-Leader Andrea Stewart-Cousins and Speaker Carl Heastie calling on elected officials to include the Ounce of Prevention Act (S1366 (2023) | A8441A (2022)) in the final State budget. The bill would reform the state’s Hospital Financial Assistance Law, enabling much-needed support to low-income families burdened by medical debt.

The letter is part of a united effort to end medical debt in New York state. You can show your support through our Phone2Action tool here.

Six percent of New Yorkers have been put into collections over medical bills, with numbers much higher for people of color in parts of the state. Nonprofit hospitals have sued more than 54,000 patients over medical debt they are unable to pay.

Many hospitals fail to offer meaningful financial assistance to their patients, despite receiving $1.1 billion dollars annually in state and federal funding to provide uncompensated care. Still others secure these funds despite failing the New York State Department of Health’s annual audits of their financial aid policies.

The Ounce of Prevention Act would add crucial patient protections to the existing Hospital Financial Assistance Law and increase the number of patients eligible to receive discounted care.

A copy of the letter can be found here.