HCFANY is thankful to have the opportunity to testify at the 2025 Joint Legislative Budget Hearing on Health. Our fully detailed written comments are here. The Executive Budget includes many proposals to help protect and enhance New Yorker’s access to affordable health coverage. However, the current federal landscape on health care access is uncertain, as proposed cuts to federal health programs could cost the State $10 billion to maintain health coverage for New Yorkers (Learn how these federal threats affect New Yorkers statewide and by Congressional District here).

The Managed Care Organization (MCO) tax revenue provides an opportunity for the State to ensure New Yorkers have access to and can afford health care. HCFANY urges the Legislature to consider alternatives to the distribution of $1.4 billion of this tax revenue, which currently does not include direct support for patients.

HCFANY recommends:

- Expanding subsidies for Child Health Plus to eliminate premium cliffs and align coverage start dates to the first day of the month of application.

This would help ensure that middle-income families can afford their children’s health insurance. Once families surpass the 400% Federal Poverty Level (FPL) income threshold, their children’s annual insurance premiums increase by around $3,000 per child. Additionally, the State should follow similar rules as Medicaid and the Essential Plan for CHP coverage start dates.

- Addressing New York’s expensive health care system.

New York is ranked second in the nation for the most health care spending per person, and HCFANY proposes three solutions to remedy this:

- Implement an independent New York Office of Health Care Affordability, like the model created in California.

- Include provisions of the Fair Pricing Act (S705|A2140) to ensure consumers and payers are charged a fair reimbursement rate for routine medical services, regardless of where the patient gets care.

- Improve patient outcomes and reduce inequities by including the provision of the Primary Care Investment Act (S1634|A1915A).

- Creating a principal reserve or a rainy-day fund to ensure New Yorker’s access to care is protected from the threats of federal cuts.

This funding could help keep lawfully present immigrants enrolled in Medicaid covered if the federal government cuts access to health insurance for this population.

- Increasing funding for consumer assistance programs like Navigators and the Community Health Advocates (CHA) program.

These are only a few initiatives that HCFANY is urging the Legislature to consider, please see our full written testimony here.

On January 14th, Governor Hochul delivered her 2025 ‘State of the State’ address. HCFANY commends the Governor for proposing sweeping protections for consumers and patients across the State. Her proposals feature many HCFANY advocacy goals falling under six categories: (1) mental health, (2) reproductive health, (3) chronic health conditions, (4) prescription drugs, (5) dental health, and (6) improving insurance coverage. Her proposals plan to:

(1) Mental Health

- Implement a teen mental health first aid program to equip youth with the ability to respond and address signs of mental health and substance use distress for themselves and their peers.

- Introduce an initiative that connects youths to critical mental health resources during state-funded after-school programs.

- Allocate new resources to strengthen compliance oversight and investigate more insurance complaints.

In New York, youth struggling with mental health has been on the rise; in 2023, 48 percent of teens experienced depressive symptoms ranging from mild (27 percent) to severe (11 percent) in New York. Through these proposed initiatives, the Governor hopes to provide basic skills for youths to support themselves and their peers and reduce the impacts of bullying and social violence. Additionally, the State aims to partner with the State University of New York to match social work graduate students with state-funded after-school programs to complete their required fieldwork and support vulnerable youths.

The current law requires insurers to offer an accessible network of providers, pay at least Medicaid rates for in-network services, and reimburse school-based mental health services at Medicaid rates. Through her proposal, the Governor hopes to improve compliance oversight and investigate and find solutions to mental health care access needs and complaints.

We commend the Governor for her continued commitment to protecting youth mental health and proposing reforms to improve coverage for mental health care.

(2) Reproductive Health

- Expand funding for reproductive health care facilities to enable renovations and equipment upgrades to help providers deliver the full range of comprehensive services.

In New York, reproductive health care facilities often lack the proper infrastructure to provide the full range of comprehensive services needed. The Governor hopes to support these facilities through the Reproductive Freedom and Equity Grant Fund and security grant funding to ensure a broader network of providers can deliver quality reproductive health care throughout the State.

HCFANY is excited to see the Governor’s continued effort to ensure New Yorkers have access to reproductive care. Earlier this year, she announced a first-in-the-nation initiative to provide 20 hours of paid leave for prenatal care for privately employed, pregnant New Yorkers, both full-time and part-time.

(3) Chronic Health Conditions

- Reduce cost barriers for Medicaid patients at high risk of major cardiovascular events, who need access to Glucagon-like petitde-1 (GLP-1) receptor agonists—more popularly known by their brand names, Wegovy or Ozempic.

- Expand eligibility for Essential Plan members to receive air conditioning units to protect themselves during severe heat events. New eligibility will cover those with diabetes, cardiovascular disease, hypertension, or those who are pregnant.

Obesity is a significant concern for New Yorkers; in 2023, around one in three New Yorkers were found to be obese. This chronic condition increases the risk of diabetes, asthma, cardiovascular disease, cancer, and other chronic health conditions. Recently, GLP-1s have transformed obesity treatment, but many face cost barriers to this life-saving treatment. The Governor proposes to provide greater access to GLP-1 drugs for Medicaid members at high risk of cardiovascular events and pressure drug companies to lower prices.

The effects of climate change have increased the severity, duration, and frequency of extreme heat events, also known as heat waves, and these events are deadly for vulnerable populations with chronic health conditions. Heat-related deaths are more likely to occur at home, highlighting the importance of home cooling access. Last year, the Governor implemented an initiative to distribute air conditioners for Essential Plan members whose asthma poses a significant medical risk. Her proposal builds upon this by expanding eligibility to more individuals whose symptoms worsen through these heat events.

HCFANY applauds the Governor’s outstanding support for New Yorkers with chronic health conditions. These initiatives build upon the first-in-the-nation diabetes initiative that HCFANY supported, eliminating co-pays for insulin covered by state-regulated insurance plans, which went into effect this year. As of 2023, 1.8 million New Yorkers have been diagnosed with diabetes, and this initiative is estimated to save eligible New Yorkers up to $1,200 per year totaling around $14 million in 2025.

(4) Prescription Drugs

- Seek approval through the Food and Drug Administration’s Section 804 Importation Program to import low-cost Canadian drugs.

- Hold pharmacy benefit managers (PBMs) and drug manufacturers for any hidden, unnecessary cost they add to drug prices.

The United States spends more on prescription drugs than any other peer country—like Australia, Canada, and France—with prices around two to four times higher for major brand-name drugs. A nationwide survey finds that 82 percent of Americans believe the cost of drugs is unreasonable, and over half of Americans worry about being able to afford their family’s prescriptions. Last year, a bill aiming to implement prescription drug importation program to lower costs (A7954A/S604) was passed in the Senate but fell short in the Assembly. Luckily, the Governor plans to participate in the Food and Drug Administration’s Section 804 Importation Program, which achieves a similar goal in importing low-cost drugs from Canada.

Additionally, the Governor is seeking to introduce a first-in-nation initiative to improve transparency and hold PBMs and drug manufacturers accountable to uncover any unnecessary costs they add to drug prices.

(5) Dental Health

- Set minimum standards for dental plans available through New York’s insurance marketplace, New York State of Health (NYSOH).

- Expand the scope of practice for dental hygienists.

- Direct health plans to improve the availability of dental care.

It is well documented that dental care is essential to oral health, yet many New Yorkers face substantial barriers to accessing essential oral health services. HCFANY is thrilled to see the Governor’s proposal announcing plans to make minimum standards for dental plans available through New York’s insurance marketplace, New York State of Health (NYSOH)—an initiative that HCFANY has been advocating for.

The Governor also aims to introduce legislation to expand the scope of practice for dental hygienists and direct health plans to improve the availability of dental care.

(6) Insurance Coverage

- Identify and address equity gaps in quality and outcome measurements for those on Medicaid Managed Care plans.

- Create an integrated care system for Medicaid patients.

- Perform a comprehensive review of the State’s network adequacy standards and increase enforcement of plan compliance.

In 1994, New York implemented Quality Assurance Reporting Requirements (QARR), which measure and report on health care quality. Though current Medicaid Managed Care (MMC) plans meet or exceed national benchmarks for quality measures, these measurements from QARR cannot identify health inequities within the population. The Governor has proposed to direct MMC plans to analyze gaps in quality and outcomes within their populations, as well as develop strategies to address gaps, including creating a value-based payment.

New York is one of the three states where Medicaid patients can enroll in a separate MMC plan for long-term care along with their medical care coverage, called a partial capitation plan. Many also have separate Medicare coverage. This fragmentation reduces the ability for effective, person-centered, coordinated care. Through her proposal, the Governor plans to work with MMC plans to increase the availability and adoption of integrated care options and limit non-integrated offerings.

Lastly, in New York, network adequacy requirements have not been updated in decades despite variations in health care access across the state. Network adequacy standards require that health plans meet basic standards for members’ access to in-network providers without unreasonable delay or excessive travel. Currently, consumers are often directed to unavailable or out-of-network providers, which leads to untimely care and an increased risk of incurring medical debt. The Governor’s proposal intends to instruct the Department of Health to perform a comprehensive review on network adequacy standards and increase enforcement of plan compliance. HCFANY supports the Governor’s continued investment in proposing initiatives that help protect consumers from incurring medical debt, an issue that HCFANY continues to advocate for.

HCFANY commends the Governor for introducing these initiatives to protect patients and consumers in New York. HCFANY will review the newly released Executive Budget to determine how these proposals will be implemented.

The season of giving is coming early for many New Yorkers seeking hospital care this year. As of last month, amendments to New York’s Hospital Financial Assistance Law (HFAL) will make it easier to apply for and cover more patients under financial assistance programs. The HFAL, also known as Manny’s Law, was implemented in 2006 in response to the death of Manny Lanza, 24. Lanza passed away after being denied life-saving surgery due to his uninsured status.

Financial assistance programs help many patients receive affordable care on a sliding fee scale based solely on their household income. This includes patients who are uninsured or those with insurance, but medical costs are a big strain on their income. Rising hospital prices in recent years have left many patients unable to afford the care they need, often leading them to incur medical debt. A 2023 Urban Institute reported that 740,000 New Yorkers had medical debt, with nearly half of them owing $500 or more. This updated HFAL will streamline the process and expand the eligibility of hospital financial assistance. New Yorkers will finally be able to have some more relief from medical debt and rising healthcare costs.

The following changes will be made to HFAL and medical debt in New York.

- All hospitals licensed by the New York State Department of Health (NYSDOH) are required to use a Uniform Hospital Financial Assistance form and inform patients of financial assistance availability in writing during registration and at discharge (regardless of the hospital’s participation in the Indigent Care Pool). Eligibility will not consider the patient’s immigration status. Before this amendment, many patients were never informed financial assistance existed and many hospitals requested information that was not legally required, like Social Security Numbers or tax returns, which often scared patients away from applying.

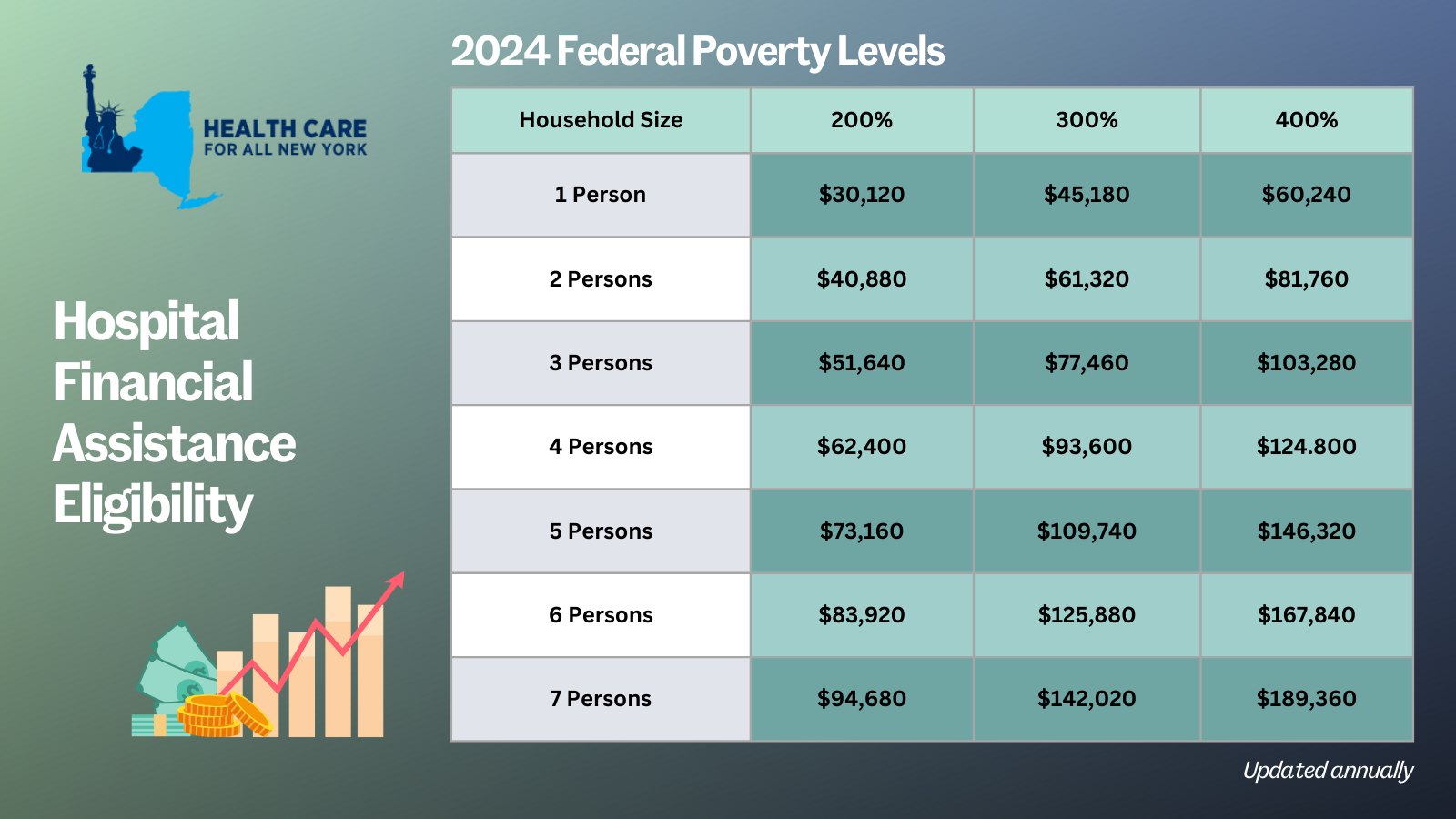

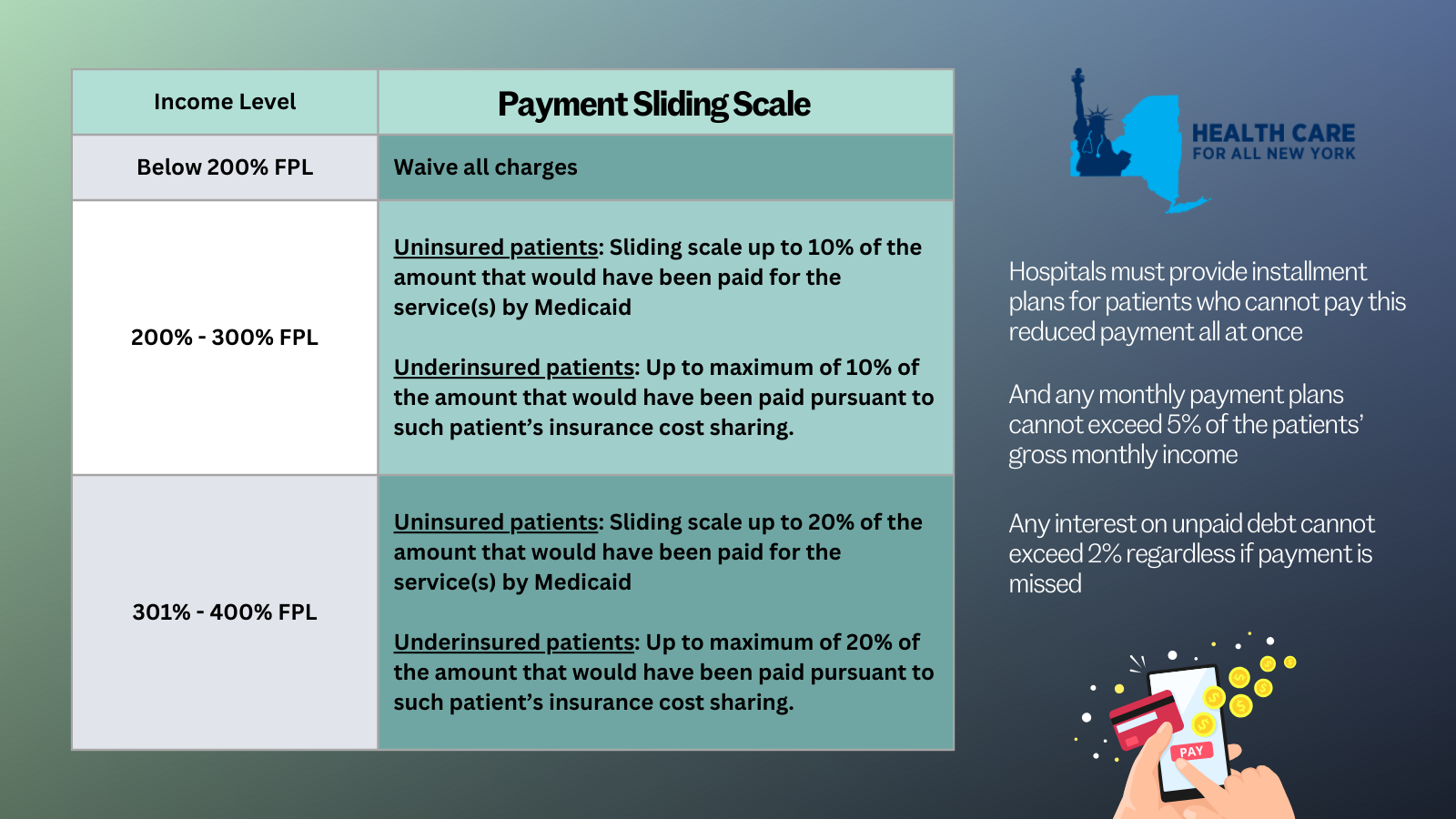

- Patient eligibility for financial assistance will be expanded for those uninsured and underinsured. Under the new law, being underinsured is defined as patients whose paid medical expenses, excluding insurance premiums, exceeds 10 percent of their income within the last 12 months. Uninsured patients will now qualify if their household earns up to 400 percent of the federal poverty level (FPL) and will receive free or discounted care based on a sliding scale (see the table below for eligibility guidelines based on household size and the payment sliding scale). These guidelines will be solely based on the FPL and are updated through the Poverty Guidelines | ASPE.

- Individuals can now apply for hospital financial assistance at any time.

- Hospitals may not sell patients’ debt to third party entities like debt collection agencies. Often these agencies use aggressive and threatening practices to make patients pay medical debt.

- Hospitals are prohibited from bringing lawsuits against patients earning up to 400 percent FPL to collect unpaid medical bills. And lawsuits to collect unpaid balances cannot be brought until 180 days after the first medical bill. Lawsuits have disproportionately affected people of color and low-income residents. For example, according to a 2024 Community Service Society of New York report, over a third of lawsuits filed by State-run hospitals were filed against patients who lived in zip codes where residents are disproportionately people of color. Additionally, nearly all these cases were filed against patients that should have been eligible for hospital financial assistance.

- To measure this impact, hospitals will report to the DOH the number of people that have applied for financial assistance annually including age, gender, race, ethnicity, and insurance status.

With this series of reforms, more New Yorkers will be able to receive affordable hospital care and reduce their chances of incurring medical debt. The HFAL was a landmark reform back in 2006 and has been far improved with these amendments.

Here’s a copy of the form hospitals must use now.

If you need assistance in applying for hospital financial assistance, contact Community Health Advocates at 888-614-5400.

New York State of Health (NYSOH) has included several exciting new initiatives in its 2025 Plan Invitation. Though some of the initiatives are subject to federal approval, HCFANY is thrilled about the improvements to the quality and affordability of health insurance plans offered on the NYSOH marketplace. Here are some key wins for consumers:

- Eliminating in-network cost-sharing for New Yorkers with diabetes in State-regulated plans. The program applies to medical care, prescription drugs, supplies, and diagnostics related to the primary diagnosis of diabetes.

- Cost-sharing subsidies for low- and moderate-income New Yorkers on Qualified Health Plans (QHP) with incomes up to 400 percent of the Federal Poverty Level (FPL), or $125,000 for a family of four. If approved, NYSOH will use $315 million of federal waiver passthrough funding that was allocated for these subsidies in the 2024-25 State Budget.

- Expanding maternal health cost-sharing initiatives to QHPs to allow pregnant and post-partum New Yorkers to access zero copay care for almost all diagnoses and services through 12 months postpartum.

- Eliminating waiting periods for standalone dental plans offered through NYSOH for all adult dental services (exception for orthodontics), allowing New Yorkers to use the coverage they are paying for.