Every year, health insurance carriers that participate in New York’s Marketplace, New York State of Health, submit requests to the Department of Financial Services (DFS) on what they would like to charge for health insurance premiums the following year. See below for template language and instructions for submitting a comment on the proposed 2027 premium increases.

Starting five days after the proposed rates are released, consumers have 30 days to submit comments. DFS considers consumer comments to determine the approved premium changes (typically increases) each insurer is allowed. This process, known as prior approval or rate review, is an opportunity for the State to keep premiums affordable for New Yorkers.

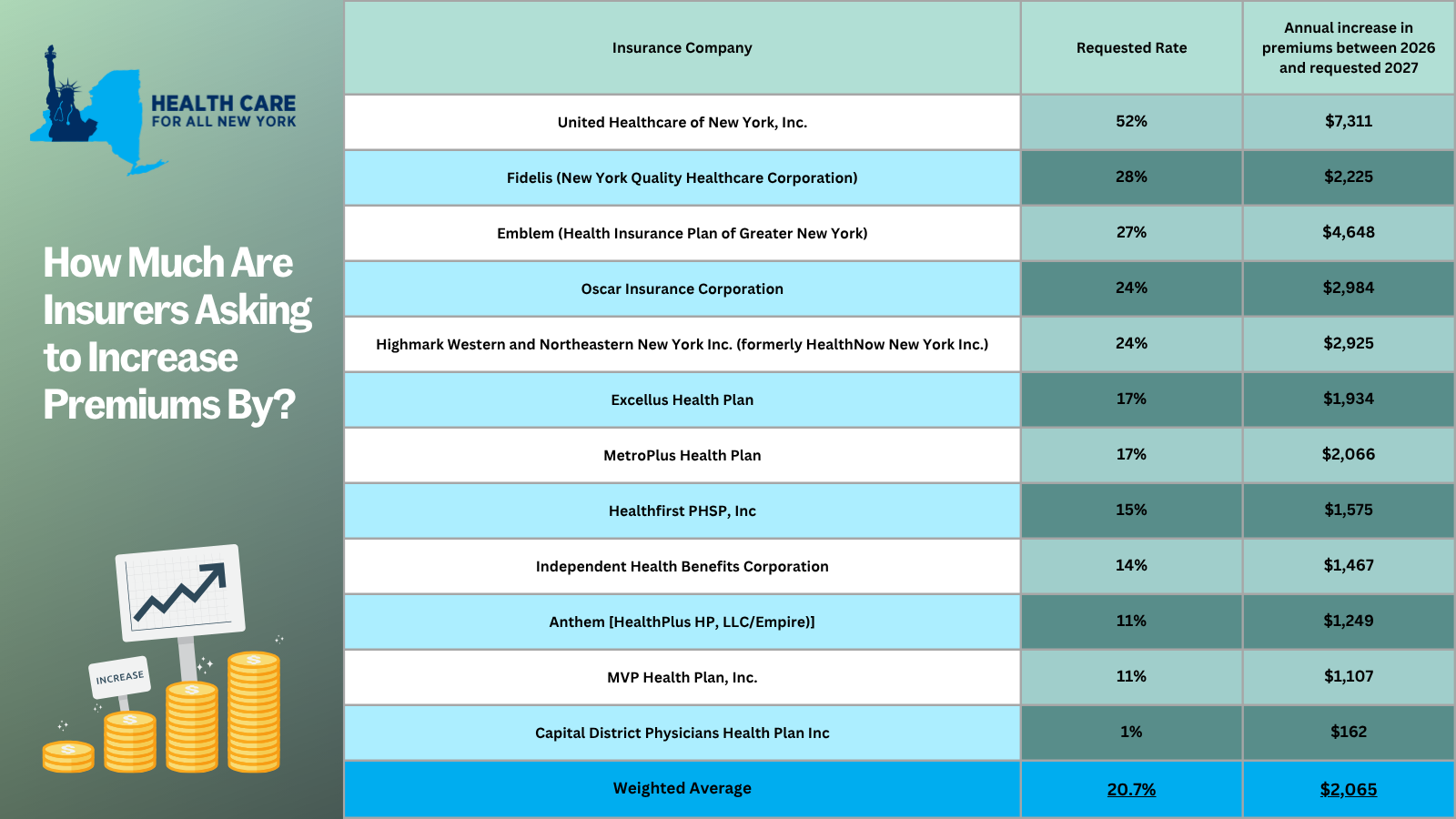

This year, New York’s individual market insurance carriers have asked the Department of Financial Services to allow them to increase premiums by an average of 21% in 2027. This increase would force New Yorkers to pay an average of $2,065 more annually, or $172 more monthly, in premiums. HCFANY hopes the State continues its trend of reducing carrier premium increase requests. For the past three years, the State has approved premium increases of 14% in 2024, 13% in 2025, and 7% in 2026.

Up until July 17th, consumers can make their voices heard by weighing in on the prior approval process.

Depending on the carrier, premiums could increase by 1% to 52% in 2027, limiting New Yorkers’ ability to spend on other essentials like groceries, transportation, or housing. Below is a table showing the breakdown by carrier.

Make your voice heard: submit a public comment before July 17th, 2026, sharing how steep premium increases would affect your budget or loved ones. Below are the steps and an example script to submit a public comment online.

- Go to https://myportal.dfs.ny.gov/web/prior-approval/submit-a-comment.

- Select the following in the drop-down boxes. This information can be found on your insurance card or plan letter notice.

- The type of plan you have

- Insurance company

- Whether you are on an Individual or group policy

- Fill in your First Name, Last Name, and Contact Information (select one of three options: Email, Address, or Phone number)

- Write a Comment (Use the example script below if you need help!)

- Comments can be very short and direct. Every comment helps demonstrate that another member will be harmed if the Department approves the carrier’s current request.

“[insert your carrier’s name] is asking for a [insert from table] % premium increase, which means an annual premium increase of [insert from table]. I cannot afford this. Back-to-back increases in premiums are absurd.

I need health insurance to [insert a reason why you need health care, like affording your prescription drugs, needing to access preventative care, or certain medical services].

At this price, I will be forced to give up [insert reason, such as childcare, groceries, or housing] or forgo health coverage. I urge you to curb these increases and consider how this will impact my family and me.”

_________________________________________________________________________________________________________

Look out for HCFANY’s comments on each carrier’s rate application in the coming weeks.

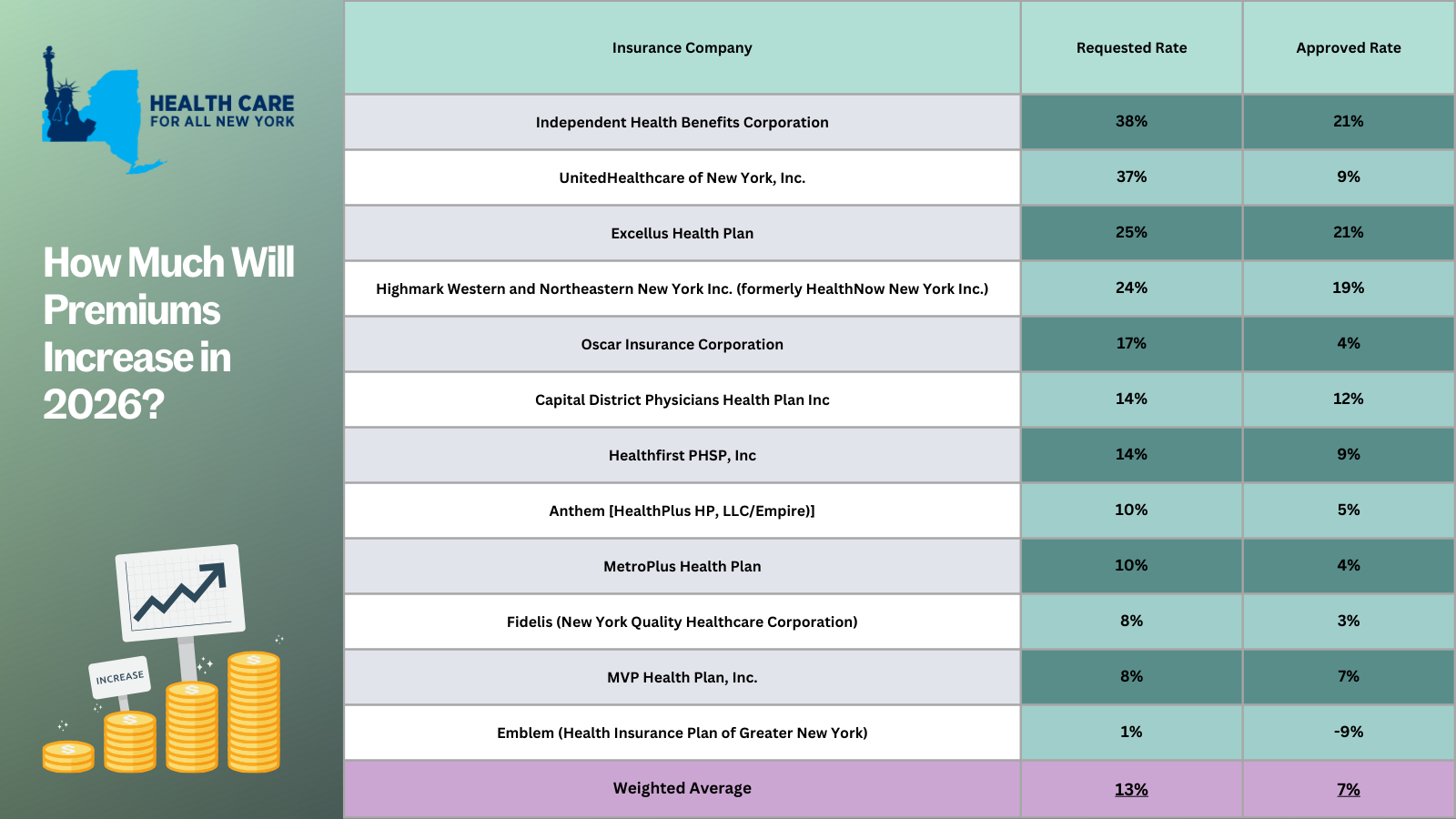

The New York Department of Financial Services (the Department) reduced the requested rates by insurance carriers for the individual market by 48 percent for 2026. Carriers initially requested a 13 percent average rate surge, but through New York’s prior approval process, the Department trimmed this figure down to an average of seven percent. Without this process, rates requested by insurance carriers would require New Yorkers to pay an average of $1,291 more annually, or $108 per month, in premiums next year. With the newly approved rates from the Department, the annual increase in premiums is now $678, or $57 per month, for next year.

The table below compares health plans’ initial rate requests with rates that were ultimately approved, providing insight into how this process impacts your health care costs (you can also review our detailed comments on each carrier’s rate request here).

The prior approval process serves as an essential safeguard to curb rising health care costs. For the past two years, the State has approved, on average, steep premium increases of 13% in 2025 and 12% in 2024. With a record number of public comments submitted by consumers, the State reduced the high premium increases requested by individual market insurance carriers. Despite these efforts, any rise in premiums for New Yorkers makes health care even less affordable for consumers, especially with current federal proposals that threaten New York’s health care system:

- Enhanced premium tax credits are set to expire at the end of this year. Unless Congress decides to extend these credits, New Yorkers—who previously received them—can expect a monthly average premium increase of $114.

- New Centers for Medicare and Medicaid Services guidance, set to take effect in 2027, will take away health coverage from 750,000 New York children, from ages 0 to 6, on Medicaid or Child Health Plus.

- The so-called “One Big, Beautiful Bill” is estimated to leave around 1.5 million New Yorkers without health coverage. Learn more about how federal threats impact the State here.

New York should consider additional strategies to protect consumers from steep premium increases beyond the rate review process. HCFANY recommends the State to implement many proposals in HCFANY’s 2025 Policy Agenda that will help patients get affordable care and coverage, like the Primary Care Investment Act, Zero-copay Inhalers, the Fair Pricing Act, or setting up an independent Office of Health Care Affordability.

Many New Yorkers, who purchase their own health coverage through the New York State of Health marketplace, are eligible for subsidies. If you need help switching plans or finding affordable health insurance, the Navigators program offers free, unbiased guidance and can help you understand your premium assistance and coverage options. You can contact Navigators through the CSS Navigator Network at 888-614-5400 or email enroll@cssny.org.

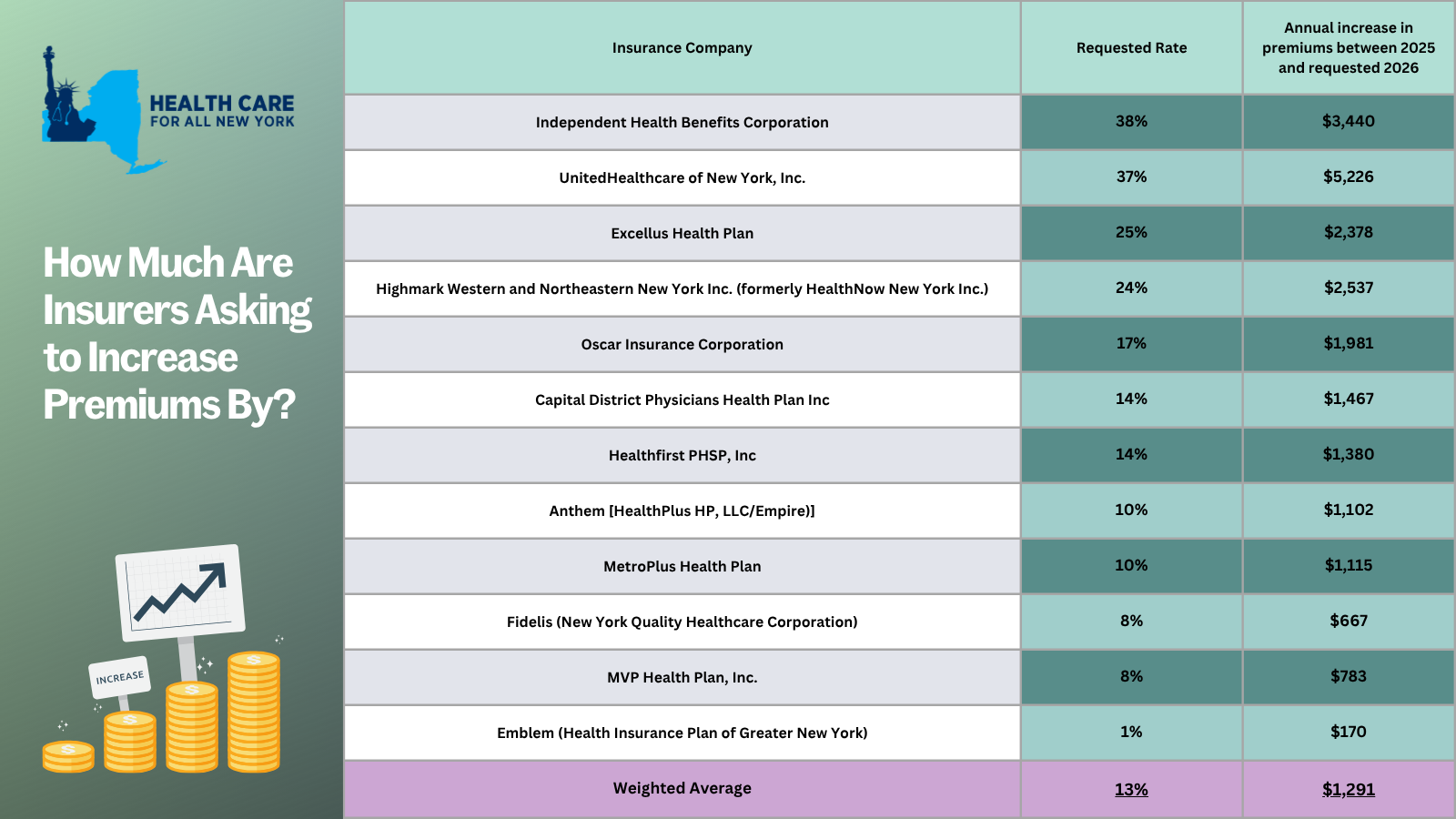

New York’s individual market premiums might increase by up to 13 percent in 2026, forcing consumers to pay an extra $1,291 more annually. New York’s twelve individual market carriers are requesting increases ranging from one percent by Emblem to a staggering 38 percent by Independent Health. These requests far surpass requests from carriers in other states.

In our comments, HCFANY breaks down why DFS should curb each carrier’s specific rate requests to protect patients from another unaffordable increase in health care costs. Find your carrier in the list below:

- Anthem

- CDPHP

- Emblem

- Excellus

- Fidelis

- Healthfirst

- Highmark

- Independent Health

- MetroPlus

- MVP

- Oscar

- United

New York’s individual market insurance carriers have asked the Department of Financial Services to allow them to increase premiums by an average of 13% in 2026. This increase would force New Yorkers to pay an average of $1,291 more annually, or $108 monthly, in premiums.

For the next 30 days, starting June 2nd, consumers can make their voices heard by weighing in on the prior approval process.

For the past two years, the State has approved a steep premium increase of 13% in 2025 and 12% in 2024. Another 13% would make health care access even more difficult to reach for many New Yorkers. This percentage increase is greater than wage growth in New York in 2024, as wages have only grown from .4% to 4.6% across the State, depending on the county.

Based on your carrier, premiums could increase between 1% and 38% in 2026, inhibiting New Yorkers’ ability to spend on other essentials like groceries, transportation, or housing. It is critical that the State hears from consumers to ensure that health insurance companies are not making health care even more unaffordable.

Make your voice heard: submit a public comment before July 1, 2025, sharing how steep premium increases would impact your budget or loved ones.

Tell the State how more expensive premiums would impact you by leaving a public comment here by Tuesday, July 1. Share a statement or story on your health care needs and affordability concerns you have, or use the following sample for guidance:

“My plan, (insert carrier name), has asked for a (insert from table below) % premium increase. This would increase my annual premiums by (insert from table below). I already struggle to afford health insurance, and that increase would require me to sacrifice ____.”