The season of giving is coming early for many New Yorkers seeking hospital care this year. As of last month, amendments to New York’s Hospital Financial Assistance Law (HFAL) will make it easier to apply for and cover more patients under financial assistance programs. The HFAL, also known as Manny’s Law, was implemented in 2006 in response to the death of Manny Lanza, 24. Lanza passed away after being denied life-saving surgery due to his uninsured status.

Financial assistance programs help many patients receive affordable care on a sliding fee scale based solely on their household income. This includes patients who are uninsured or those with insurance, but medical costs are a big strain on their income. Rising hospital prices in recent years have left many patients unable to afford the care they need, often leading them to incur medical debt. A 2023 Urban Institute reported that 740,000 New Yorkers had medical debt, with nearly half of them owing $500 or more. This updated HFAL will streamline the process and expand the eligibility of hospital financial assistance. New Yorkers will finally be able to have some more relief from medical debt and rising healthcare costs.

The following changes will be made to HFAL and medical debt in New York.

- All hospitals licensed by the New York State Department of Health (NYSDOH) are required to use a Uniform Hospital Financial Assistance form and inform patients of financial assistance availability in writing during registration and at discharge (regardless of the hospital’s participation in the Indigent Care Pool). Eligibility will not consider the patient’s immigration status. Before this amendment, many patients were never informed financial assistance existed and many hospitals requested information that was not legally required, like Social Security Numbers or tax returns, which often scared patients away from applying.

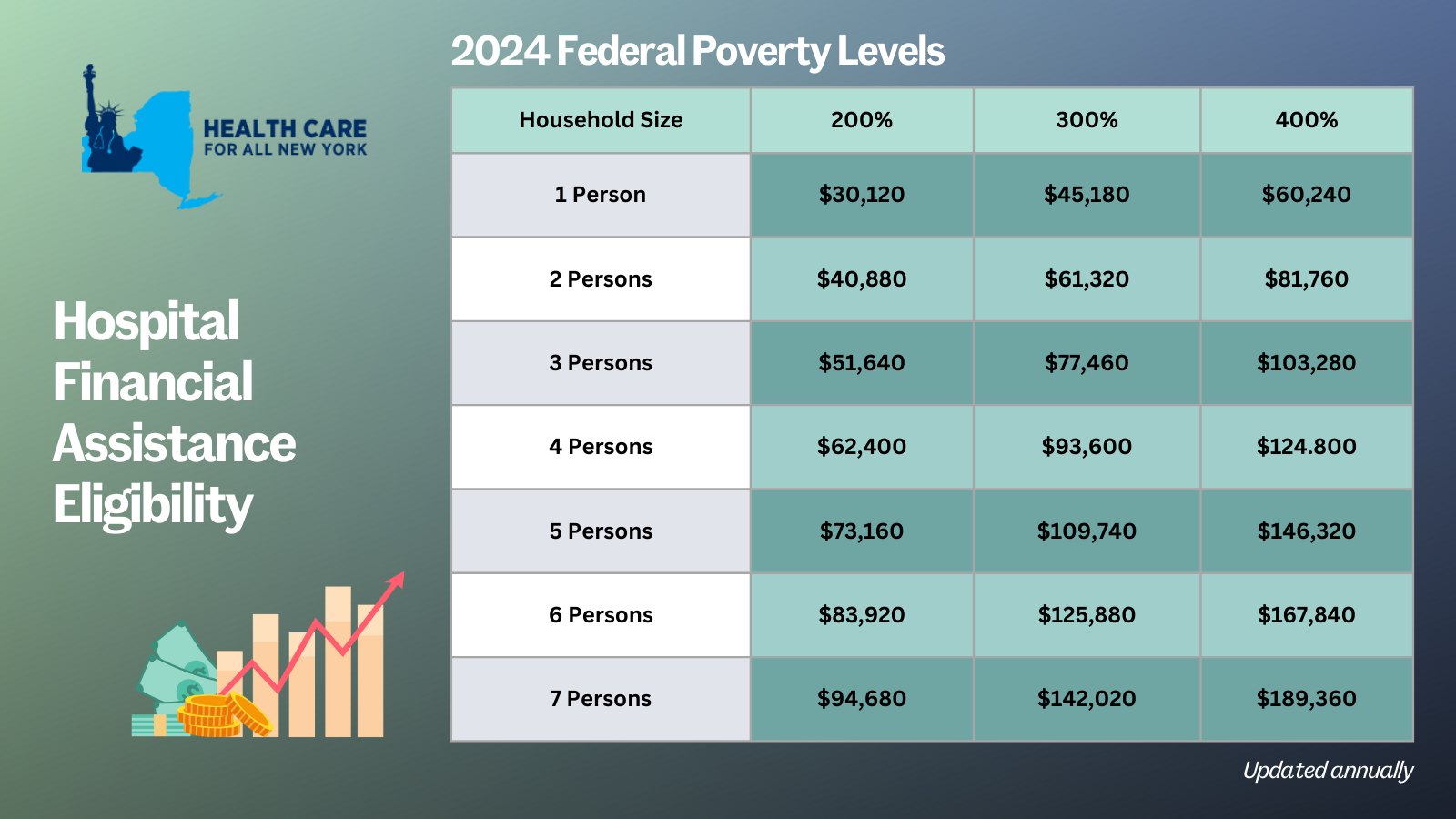

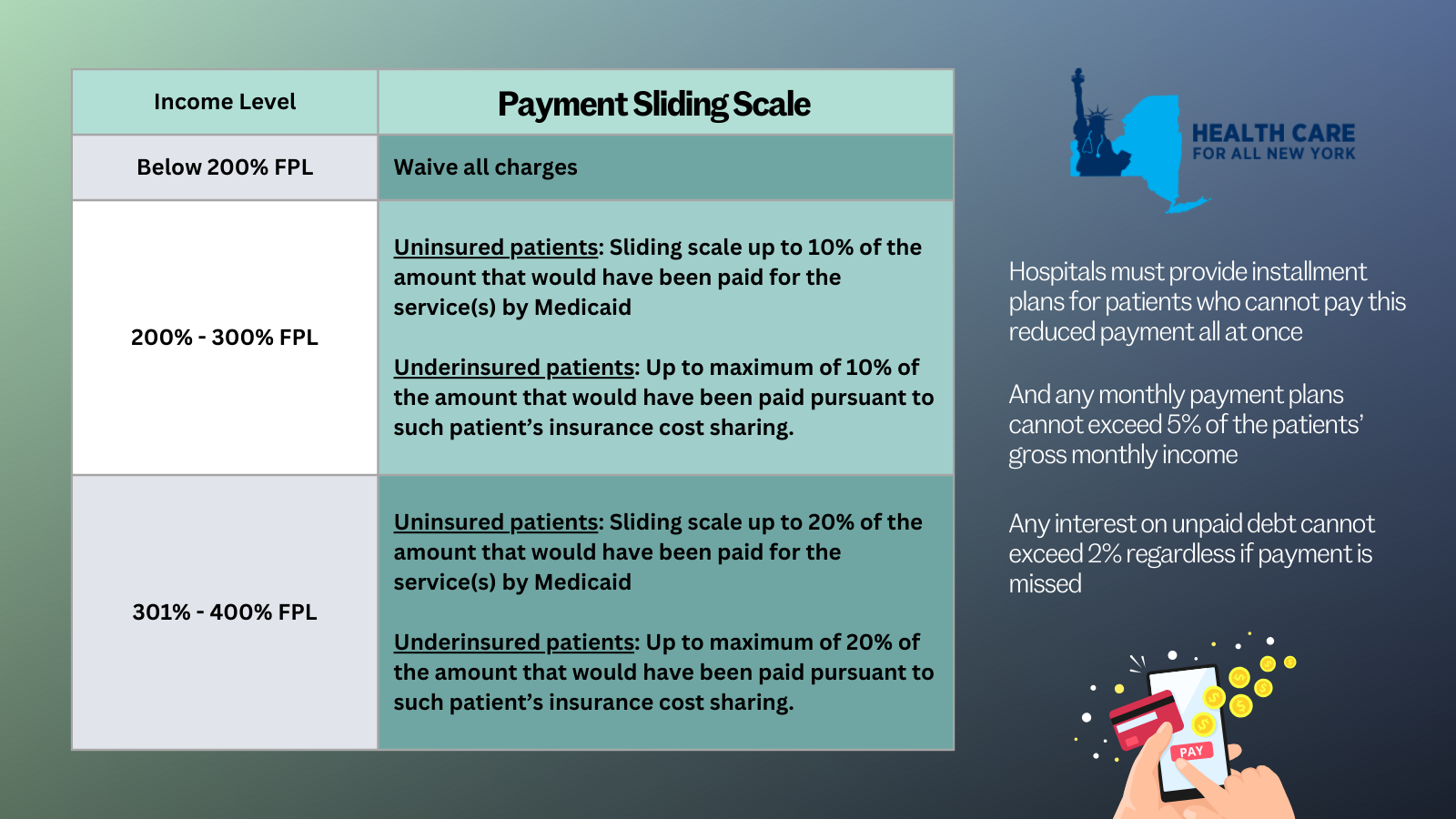

- Patient eligibility for financial assistance will be expanded for those uninsured and underinsured. Under the new law, being underinsured is defined as patients whose paid medical expenses, excluding insurance premiums, exceeds 10 percent of their income within the last 12 months. Uninsured patients will now qualify if their household earns up to 400 percent of the federal poverty level (FPL) and will receive free or discounted care based on a sliding scale (see the table below for eligibility guidelines based on household size and the payment sliding scale). These guidelines will be solely based on the FPL and are updated through the Poverty Guidelines | ASPE.

- Individuals can now apply for hospital financial assistance at any time.

- Hospitals may not sell patients’ debt to third party entities like debt collection agencies. Often these agencies use aggressive and threatening practices to make patients pay medical debt.

- Hospitals are prohibited from bringing lawsuits against patients earning up to 400 percent FPL to collect unpaid medical bills. And lawsuits to collect unpaid balances cannot be brought until 180 days after the first medical bill. Lawsuits have disproportionately affected people of color and low-income residents. For example, according to a 2024 Community Service Society of New York report, over a third of lawsuits filed by State-run hospitals were filed against patients who lived in zip codes where residents are disproportionately people of color. Additionally, nearly all these cases were filed against patients that should have been eligible for hospital financial assistance.

- To measure this impact, hospitals will report to the DOH the number of people that have applied for financial assistance annually including age, gender, race, ethnicity, and insurance status.

With this series of reforms, more New Yorkers will be able to receive affordable hospital care and reduce their chances of incurring medical debt. The HFAL was a landmark reform back in 2006 and has been far improved with these amendments.

Here’s a copy of the form hospitals must use now.

If you need assistance in applying for hospital financial assistance, contact Community Health Advocates at 888-614-5400.

Health Care for All New York is delighted that the new budget deal includes key HCFANY legislative agenda items, including: the reform of our State’s broken Hospital Financial Assistance Law (HFAL); the elimination of cost-sharing for insulin; a program to provide enhanced subsidies to help offset the costs or premiums of cost-sharing in the Marketplace; and continuous coverage for children up to age six in our State’s public health insurance programs. But HCFANY is hugely disappointed to see that Coverage4All was not included in the final deal. And in a break with the Assembly’s historic support for Community Health Advocates, it maintained over a 50 percent cut to its allocation ($1 million in 2023 decreased to $469,000 in 2025).

The Budget deal reforming our state’s broken HFAL will provide enormous relief to New Yorkers. Over the past 7 years, New York’s “charitable” hospitals have sued over 80,000 patients contributing to the grim statistic that 760,000 people have medical debt. The ubiquity of these lawsuits will now be significantly curtailed. The new law outright bans lawsuits against patients with incomes below 400% of the federal poverty level (FPL), which is about $60,000 for an individual. It also requires hospitals to provide free care to patients with incomes up to 200% of FPL ($30,000 for an individual), and heavily discounted care – between 10-20% of the Medicaid rate – for patients up to 400% of FPL. Further, hospital payment plans cannot charge more than 5% of a patient’s gross family income in a year. And it eliminates burdensome “asset” test rules that became a cover for bureaucratic applications where patients have to prove the negative: that they are not secretly stashing their wealth in an effort to get help paying for healthcare. Finally, hospitals will be barred from including “immigration” eligibility tests for financial assistance.

Another positive aspect of the budget for healthcare consumers is the inclusion of a law that eliminates cost-sharing for insulin for enrollees in state-regulated health insurance plans. More than 1.5 million New Yorkers have diabetes, of which about 500,000 people rely on insulin. This provision will help many diabetics, but especially people of color, seniors, and people who live in low-income households, who disproportionately suffer from diabetes complications, including kidney failure, blindness, and loss of limbs.

Two key coverage provisions were also included in the final budget. First, New York will join the states of Oregon and Washington to guarantee continuous public insurance (Medicaid and Child Health Plus) coverage of children up to the age of six. This provision will help families avoid costly gaps in health coverage. Second, the budget includes authorization to improve cost-sharing or premium assistance programs for people enrolling through the Marketplace. Few details are out, but HCFANY will post about these measures as they are finalized.

While the Budget news is mostly good, HCFANY is hugely disappointed that the Assembly Leadership has broken with its storied tradition of standing up for healthcare consumers in two important areas. First, the Budget deal failed to include Coverage4All, a foregone conclusion by the Assembly’s omission in its one-house budget bill. Second, the Assembly continued to maintain over a 50% cut in its share of funding for the Community Health Advocates program which serves over 35,000 consumers a year, saving them $36 million in health care costs.

Our work is not done! For the remainder of the session, which ends on June 6, HCFANY will focus on trying to secure the passage of the stand-alone Coverage4All bill (S2237B|A3020), which would authorize the Governor to amend the 1332 Waiver to secure funding for covering up to 150,000 immigrant New Yorkers, as well as the “Stop SUNY Suing” Act (A8170|S7778), which would prevent the five state-operated hospitals from suing their patients with medical debt.

One Pager: New York’s Reformed HFAL

Over a decade ago, New York State enacted Manny’s Law, which required New York’s non-profit hospitals to provide hospital financial assistance to low-income patients. The law is named after Manny Lanza, a young New Yorker with a brain condition who died after being precipitously discharged from a hospital because he was uninsured. Under Manny’s Law, hospitals must provide financial assistance to uninsured, low-income patients in exchange for receiving funds from the State’s $1.1 billion Indigent Care Pool. In 2012, the Department of Health began to audit the hospitals’ financial aid programs in response to reports of inadequate compliance.

A Freedom of Information Law request filed with the Department of Health shows that a decade later, hospitals still fail to comply with Manny’s Law—and, in fact, appear to be regressing, with the audit showing that they were less compliant in 2018 than they were the prior two years. The audit includes a list of questions that hospitals can pass or fail, and the chart below shows the total number of failed questions:

What kinds of problems did the audit reveal?

First, the audit found that a decade after the passage of Manny’s Law, many hospitals’ financial aid applications still include impermissible requirements that make it hard for patients to apply. For example, 17% of hospitals audited had incorrectly adopted a “Medicaid denial first” policy. Medicaid applications can take a lot of time to process. Requiring a patient to receive a denial before beginning the financial assistance process causes unnecessary delay for patients. Other impermissible hurdles to hospital financial aid revealed by the audit included requiring patients to provide their: past tax returns (14.3%); monthly bills and other financial obligations (13.1%); and Social Security numbers (12.0%).

Second, the audit found that many hospitals’ financial assistance policies do not protect low-income patients from extraordinary collections actions that are explicitly forbidden under state law because they are so harmful to patients. For example, one in five hospitals said that they allow accelerator clauses that mean missed payments trigger higher rates of interest (20.0%). Interest adds hundreds or thousands of dollars to medical bills that patients are already struggling to pay. (A bill to reform New York State’s onerous 9 percent judgment interest rate awaits Governor’s Hochul’s signature (S55724B/6474B).) Next, the audit reveals that hospitals are allowing collections agencies to pursue their patients without the hospitals’ written consent (9.1%). This means patients are hassled by debt collectors even while they are working on applying for financial assistance or otherwise trying to work with the hospital to pay their bill. Finally, hospitals’ policies do not explicitly prohibit forced sales or foreclosures on patients’ homes (7.4%).

Third, the audit found that hospitals apply asset tests when determining discounts, which is not allowed in almost any other health care affordability program in the state. And hospitals report that they continue to consider assets that the law says they are not allowed to consider, including a patient’s home (10.9%), retirement accounts (9.7%), college savings accounts (8.0%), and cars that anyone in the patients’ immediate family uses for their primary transportation (8.0%). This failure to comply with the law means eligible patients are denied help or are prevented from applying.

These failures to comply have serious consequences for patients who should have been protected by Manny’s Law and offered care at discounted rates. According to a 2019 poll, 45 percent of New Yorkers say they delay or avoid health care altogether because they cannot afford it. Thirty-five percent of New Yorkers say that obtaining necessary health care meant serious financial struggles such as using up all of their savings, being unable to pay for food or heat, and racking up large amounts of credit card debt. Over 52,000 New Yorkers have been sued by hospitals over medical bills they cannot afford over the past five years. Hospitals then place liens on patients’ homes and garnish their wages.

Make Manny’s Law a Reality: Fix the Hospital Financial Assistance Law

What should New York do about this? One simple change is to require hospitals to use one standard application form to be developed by the state. This would obviate the need for the Health Department’s audits of a failing system that lets every hospital design and implement its own policy. Other states already do something like this. For example, Massachusetts uses its state Marketplace to award hospital financial assistance. Advocates have recommended the adoption of a single application form for years and so has the Department of Financial Services Health Care Administrative Simplification Workgroup – a multi-stakeholder group of healthcare experts. It was also proposed in last year’s Patient Medical Debt Protection bill.

After all these years, patients need our healthcare system to be simpler and more accessible. That remains the unfulfilled goal of Manny’s Law. Adopting one uniform statewide Hospital Financial Assistance form, to be used by all of New York’s hospitals, would be an important first step in leveling the playing field between patients and healthcare providers.

There are lots of opportunities coming up over the next couple of weeks to learn more about health policy priorities and how to take action. Here’s a few of them!

TODAY: Statewide Day of Action for Guaranteed Healthcare (link)

The Campaign for New York Health is holding a day of action for the New York Health Act, which would provide comprehensive health coverage for everyone who lives or works full-time in New York. Look for #PassNYHealth to see what people are saying and join in!

- Learn more about why we need the New York Health Act here.

- If you missed the day of action you can always show your support for the New York Health Act by clicking this link and telling your State Assemblymember and Senator to support the bill. If they already do, the link will give you an opportunity to thank them!

Tomorrow: #Coverage4All Virtual Day of Action

There are 400,000 New Yorkers without insurance because of their immigration status. A1585/S2549 would guarantee that all New Yorkers can access life-saving health coverage if they have had COVID-19. Look for #Coverage4All and #PassA1585 all day tomorrow to help get the word out!

What else can you do?

- Sign up for campaign updates here.

- Become listed as a supporting organization here.

- Contact your legislator any time using the instructions here.

Friday, 11:00-12:00: Budget Briefing for Health Justice Advocates

Join the Campaign for NY Health, the Consumer Directed Personal Assistance Association of New York State, Coverage4All, Health Care for All NY, and Medicaid Matters NY for an overview of the FY22 Executive Budget Proposal and its implications for healthcare in New York. Register here.

Friday, February 5 1:00-3:00: HCFANY Annual Meeting

What can we expect from legislative session this year? How do we push forward and ensure quality, affordable health care for everyone in New York State during a pandemic and a budget crisis? Join us to learn more about our legislative and budget priorities for 2021 and how you can take action yourself! Click here to register!

During this virtual meeting we will:

- Award Senator Gustavo Rivera as this year’s Consumer Champion and present a posthumous Lifetime Achievement award to Kristin Sinclair, Director of the Senate Health Committee.

- Share information about the state budget and our legislative priorities, including expanding health coverage to all New Yorkers, ending medical debt, and addressing systemic inequity in our health care system.

- Talk about future workshops that will offer deep dives on different health policy issues and opportunities to take action.