Read HCFANY’s 2024 Rate Review Comments

July, 5 2023 | by Mia Wagner

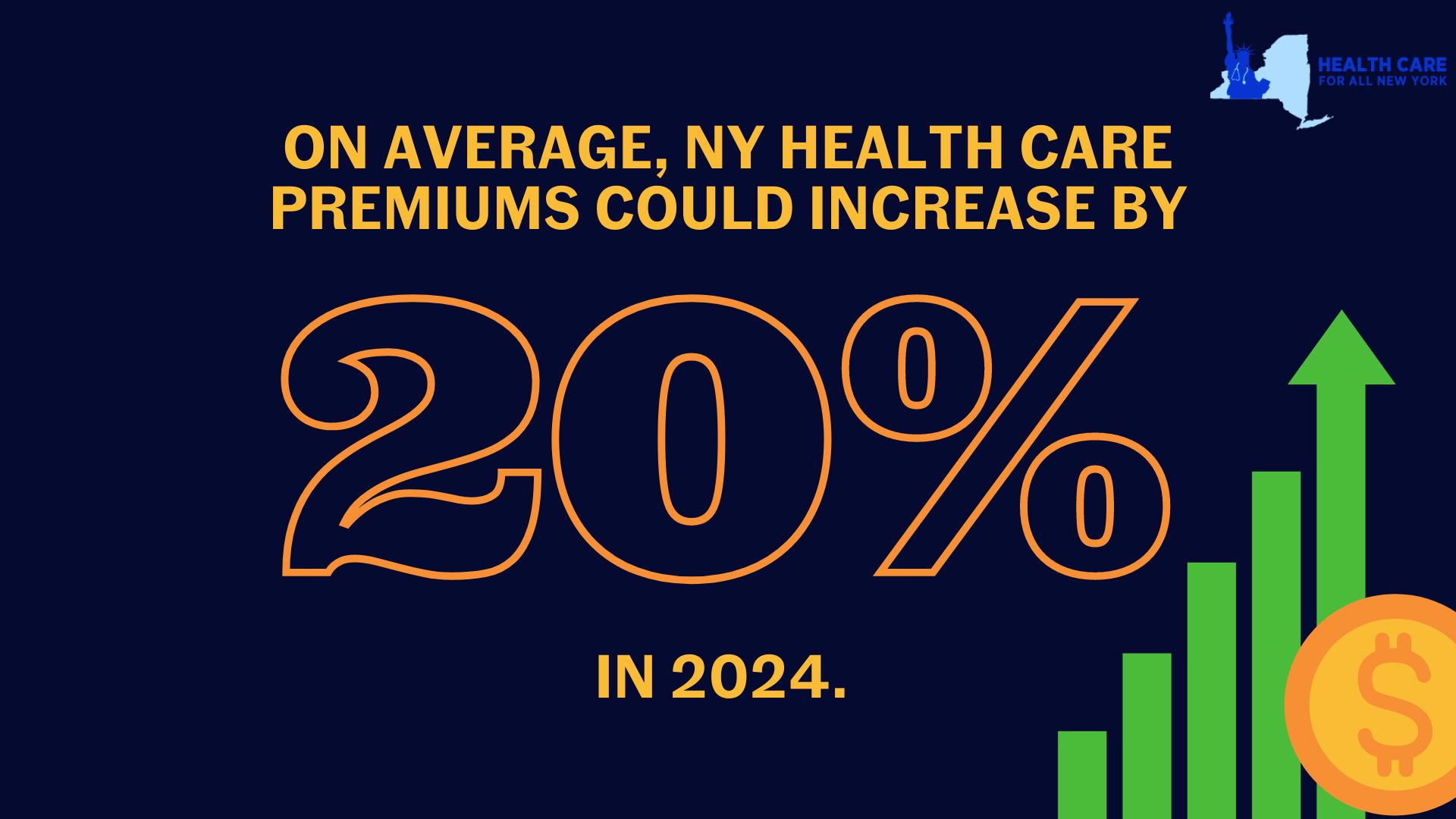

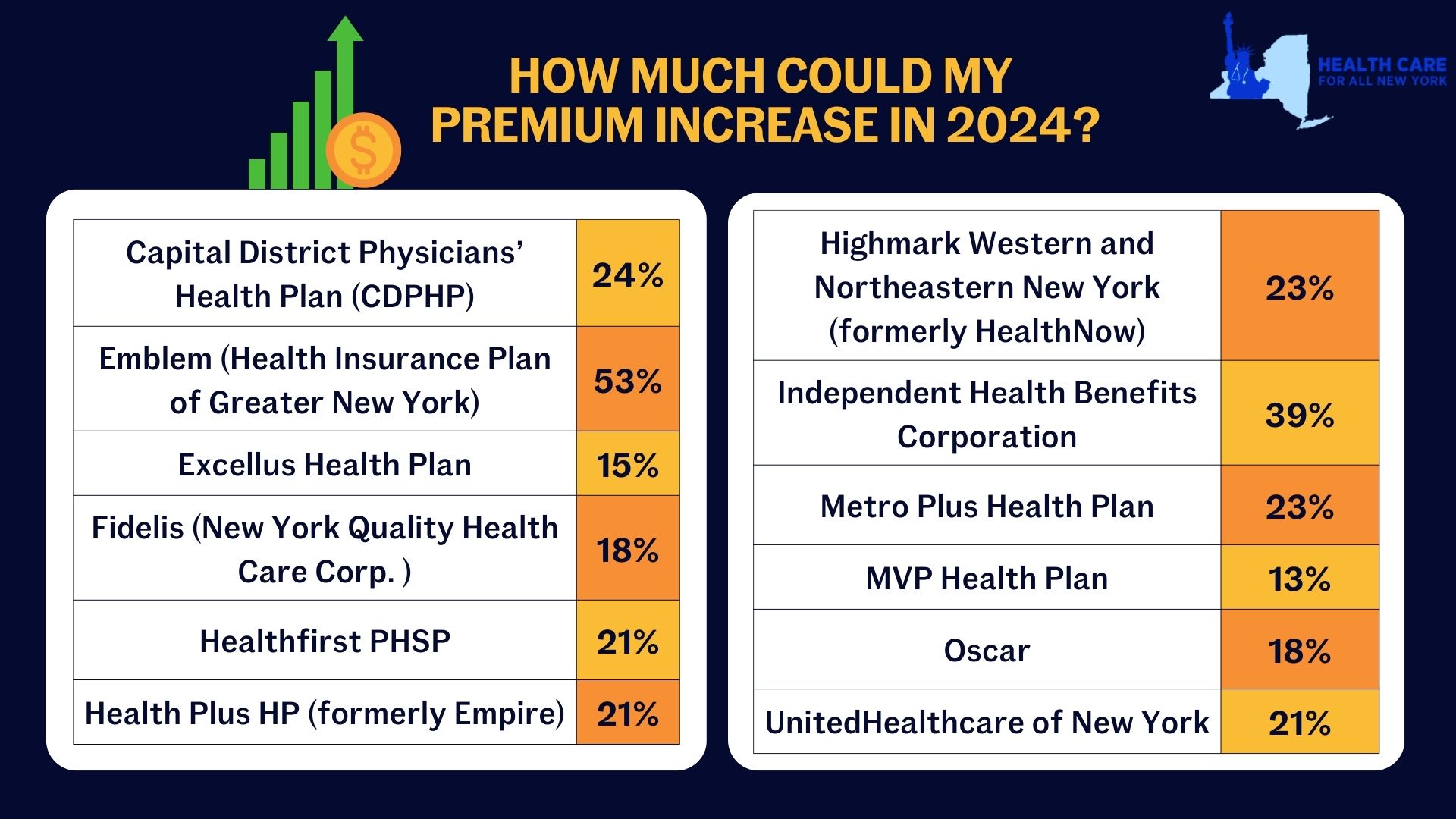

New York’s individual market premiums might increase by up to 20.4 percent in 2024. New York’s twelve individual market carriers are requesting increases ranging from 13.3 percent by MVP to a shocking 52.8 percent by Emblem. These requested increases far surpass requests from carriers in other states. Carriers in Washington and Michigan are proposing increases of just 9 percent and 5 percent respectively, despite having comparable individual markets.

Rate increases mean New Yorkers would spend a greater share of their budget on health care and less on food, transportation, and other necessities. New York insurance carriers have not offered adequate justification to support their exceedingly large requested price hikes, citing several market wide trends as rationale:

- End of the Covid-19 Public Health Emergency (PHE) – During the pandemic, New York stopped requiring people in public health insurance programs to renew (which requires verifying income). In the first two years of the pandemic, over 60,000 people left the individual market as they became eligible for Medicaid and the Essential Plan. Altogether 9.3 million New Yorkers are now renewing their coverage for the first time since 2020 and are doing so in an economy that is improved. Renewal over the next year will reveal higher incomes for many people, making them no longer eligible for public coverage and leaving them to return to the individual market. Based on enrollments so far, that could be 70,000 new people in the individual market. More people in the market should mean reduced premiums, and the Department should implement a uniform reduction to all carriers requested 2024 premium rates.

- Covid-19 Testing and Vaccination Costs – Spending on of Covid-19 treatment in 2024 is expected to be significantly lower than previous years because of the combined reduction in frequency and severity of Covid-19 cases in New York. Further, utilization is likely to decline because cost-sharing for Covid-19 testing and treatment is back, effective May 2023. Extensive research documents that even small amounts of cost-sharing reduce health care utilization. The Department should reduce the requested premiums to accurately reflect the change in costs and utilization of Covid-19 related services by individual market consumers in the 2024 plan year.

- 1332 State Innovation Waiver – The Waiver, which was filed with the federal government in May 2023, seeks to expand the Essential Plan from its current income eligibility cap from 200 to 250 percent of the federal poverty level. It is unlikely that all the procedural steps necessary to implement the Waiver will occur before the start of 2024. Given this uncertain timing, any adjustment for the Waiver should be delayed until 2025 when the State has certainty about whether the Waiver has been approved and when it is implemented.

In our comments, HCFANY breaks down why DFS should curb each carrier’s specific rate requests to protect patients from another unaffordable increase in health care costs. Find your carrier in the list below to see what we had to say:

- Independent Health

- MetroPlus

- CDPHP

- Emblem

- Excellus

- Fidelis

- Healthfirst

- Highmark

- HealthPlus

- MVP

- Oscar

- United

Tell the State how higher health care costs would impact you here. You can also tell DFS Superintendent Adrienne Harris or Deputy Superintendent John Powell to lower rates on social media by tagging @NYDFS.