The season of giving is coming early for many New Yorkers seeking hospital care this year. As of last month, amendments to New York’s Hospital Financial Assistance Law (HFAL) will make it easier to apply for and cover more patients under financial assistance programs. The HFAL, also known as Manny’s Law, was implemented in 2006 in response to the death of Manny Lanza, 24. Lanza passed away after being denied life-saving surgery due to his uninsured status.

Financial assistance programs help many patients receive affordable care on a sliding fee scale based solely on their household income. This includes patients who are uninsured or those with insurance, but medical costs are a big strain on their income. Rising hospital prices in recent years have left many patients unable to afford the care they need, often leading them to incur medical debt. A 2023 Urban Institute reported that 740,000 New Yorkers had medical debt, with nearly half of them owing $500 or more. This updated HFAL will streamline the process and expand the eligibility of hospital financial assistance. New Yorkers will finally be able to have some more relief from medical debt and rising healthcare costs.

The following changes will be made to HFAL and medical debt in New York.

- All hospitals licensed by the New York State Department of Health (NYSDOH) are required to use a Uniform Hospital Financial Assistance form and inform patients of financial assistance availability in writing during registration and at discharge (regardless of the hospital’s participation in the Indigent Care Pool). Eligibility will not consider the patient’s immigration status. Before this amendment, many patients were never informed financial assistance existed and many hospitals requested information that was not legally required, like Social Security Numbers or tax returns, which often scared patients away from applying.

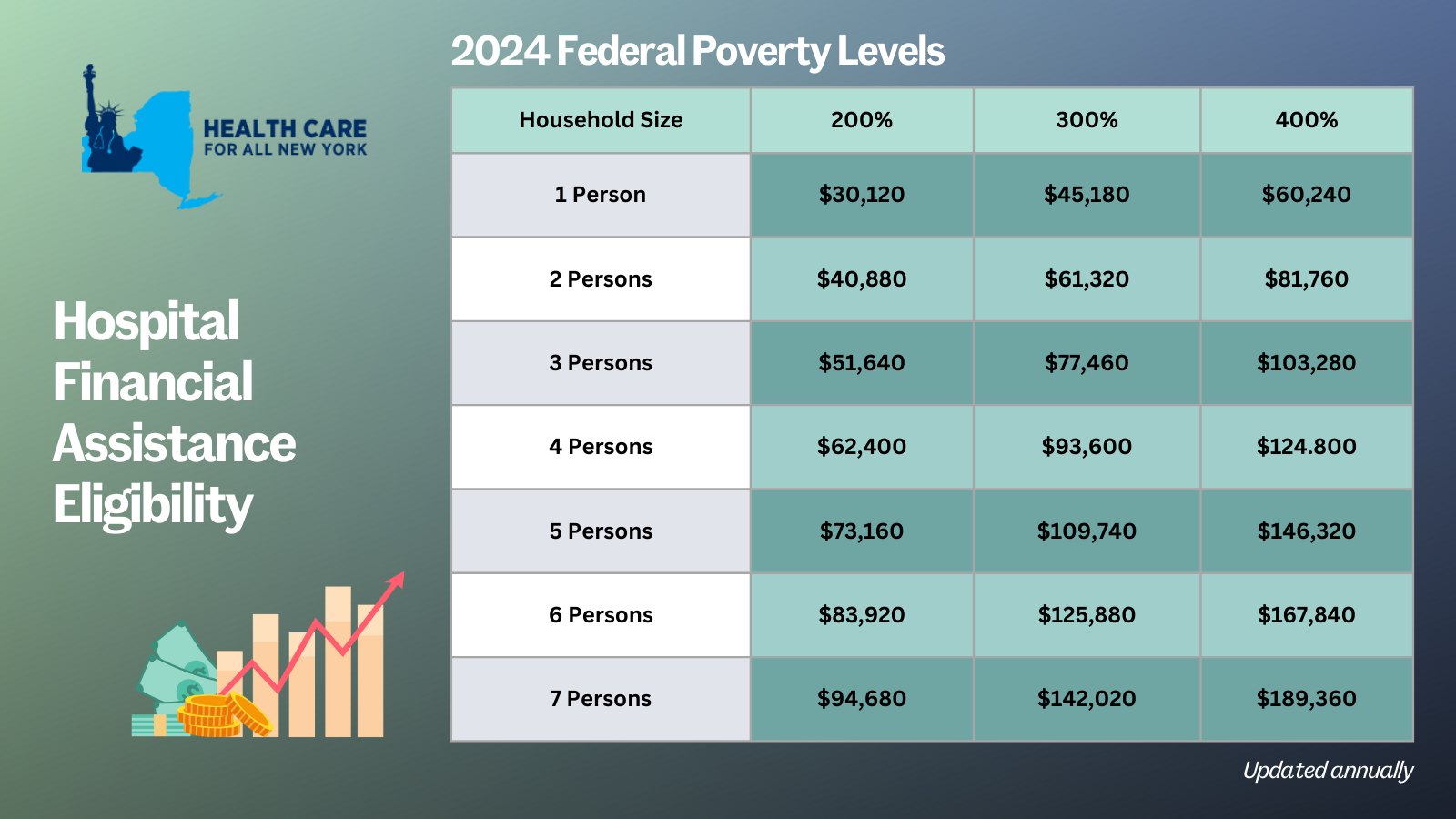

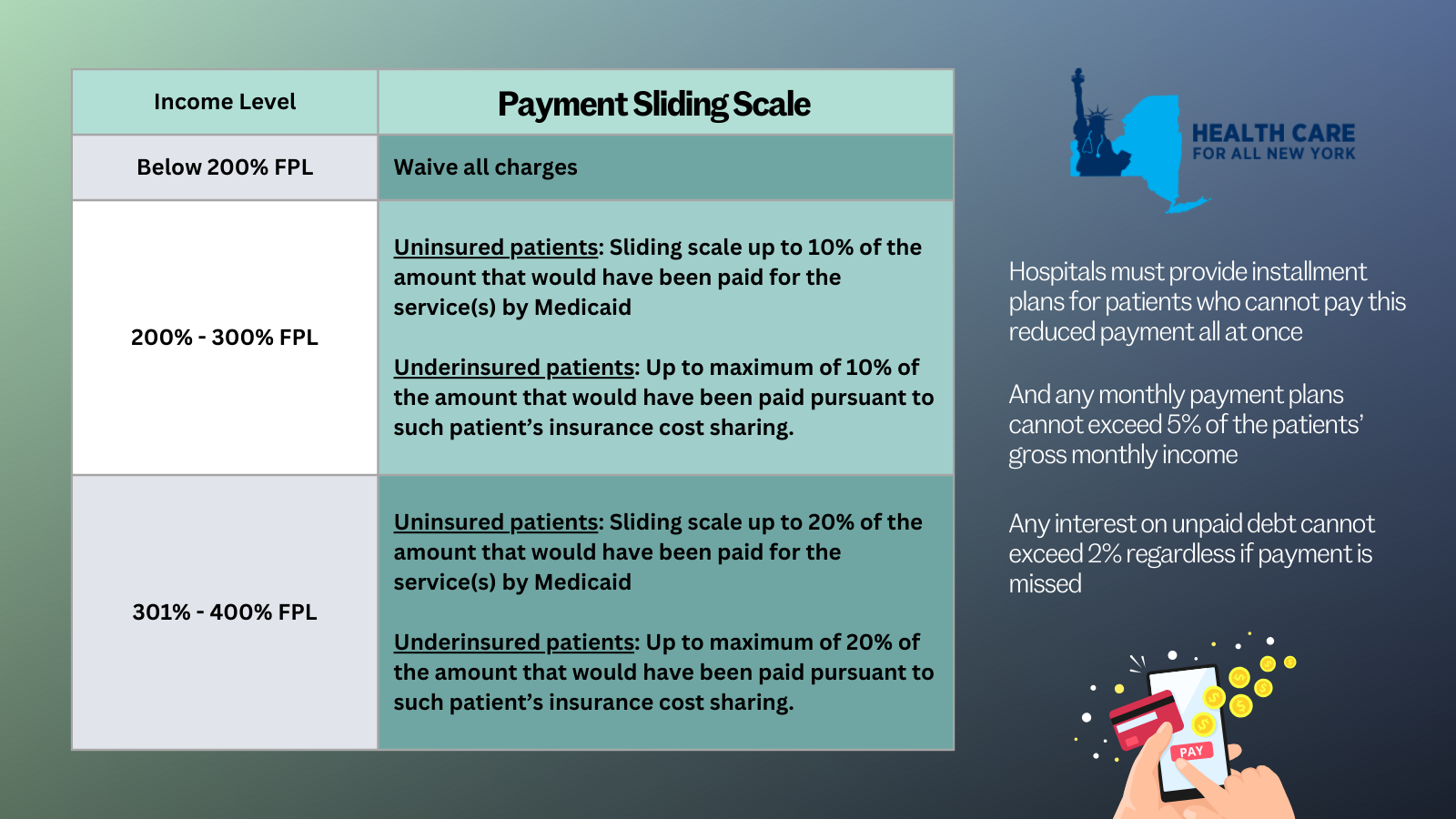

- Patient eligibility for financial assistance will be expanded for those uninsured and underinsured. Under the new law, being underinsured is defined as patients whose paid medical expenses, excluding insurance premiums, exceeds 10 percent of their income within the last 12 months. Uninsured patients will now qualify if their household earns up to 400 percent of the federal poverty level (FPL) and will receive free or discounted care based on a sliding scale (see the table below for eligibility guidelines based on household size and the payment sliding scale). These guidelines will be solely based on the FPL and are updated through the Poverty Guidelines | ASPE.

- Individuals can now apply for hospital financial assistance at any time.

- Hospitals may not sell patients’ debt to third party entities like debt collection agencies. Often these agencies use aggressive and threatening practices to make patients pay medical debt.

- Hospitals are prohibited from bringing lawsuits against patients earning up to 400 percent FPL to collect unpaid medical bills. And lawsuits to collect unpaid balances cannot be brought until 180 days after the first medical bill. Lawsuits have disproportionately affected people of color and low-income residents. For example, according to a 2024 Community Service Society of New York report, over a third of lawsuits filed by State-run hospitals were filed against patients who lived in zip codes where residents are disproportionately people of color. Additionally, nearly all these cases were filed against patients that should have been eligible for hospital financial assistance.

- To measure this impact, hospitals will report to the DOH the number of people that have applied for financial assistance annually including age, gender, race, ethnicity, and insurance status.

With this series of reforms, more New Yorkers will be able to receive affordable hospital care and reduce their chances of incurring medical debt. The HFAL was a landmark reform back in 2006 and has been far improved with these amendments.

Here’s a copy of the form hospitals must use now.

If you need assistance in applying for hospital financial assistance, contact Community Health Advocates at 888-614-5400.

New Yorkers bracing for health insurance premiums in the individual market are in for some unwelcome news as we look ahead to 2024. According to the latest data, individual market rates are set to surge by an average of 12.4 percent next year. Health plans had initially requested a whopping 22.1 percent average rate hike for 2024, but the Department of Financial Services has managed to trim down this figure through New York’s prior approval process.

The table below presents a comparison of the health plans’ original rate hike requests and the rates that were ultimately approved, giving you insight into how the process affects your healthcare costs. (Feel free to refer to our detailed comments on each rate request.)

The prior approval process serves as a critical safeguard; however, the 12.4 percent increase still poses a financial challenge for many New Yorkers. It underscores the need for New York to explore additional measures to protect consumers from steep premium rises outside of the rate review process. States like Connecticut, Delaware, Massachusetts, Nevada, New Jersey, Oregon, Rhode Island, and Washington have already taken steps in this direction, establishing Health Care Cost Containment task forces or agencies.

For those concerned about the affordability of health insurance, there’s some relief to be found. Most New Yorkers purchasing their own health coverage qualify for subsidies that can help offset premium costs. To explore your options and find out more about available subsidies, head over to the NY State of Health enrollment site. If you need assistance with switching plans or enrolling in affordable health insurance, the Navigator program is here to help. Navigators provide free, unbiased enrollment assistance and can help you understand your eligibility for premium assistance and your coverage options. You can reach out Navigators in the CSS Navigator Network at 888-614-5400 or drop them an email at enroll@cssny.org. You can reach out to assistors with the NY State of Health online here or call at 855-355-5777.

| 2024 Individual Market Rate Changes | |||

| Plan | Requested Increase | Approved Increase | Change |

| Emblem/HIP | 52.7% | 25.1% | -52.4% |

| IHBC | 39.2% | 25.3% | -35.5% |

| MetroPlus | 26.4% | 17.6% | -33.3% |

| CDPHP | 23.5% | 12.1% | -48.5% |

| Highmark | 22.6% | 13.0% | -42.5% |

| Healthfirst | 20.9% | 12.5% | -40.2% |

| UnitedHealthcare | 20.9% | 12.2% | -41.6% |

| Anthem (Formerly Empire HealthPlus) | 20.7% | 8.6% | -58.5% |

| Oscar | 18.4% | 7.9% | -57.1% |

| Excellus | 15.2% | 12.2% | -19.7% |

| MVP | 13.3% | 6.5% | -51.1% |

| Overall | 22.1% | 12.4% | -43.9% |

Transgender people across the country face discrimination and other barriers to care which can make it difficult to achieve their health care goals. These barriers are there for New Yorkers, too, and came up during a HCFANY-led focus group looking into how LGBTQ+ New Yorkers are affected by medical debt. Participants described high medical bills after coverage denials for gender-affirming care – despite plans covering these same procedures, like hormone therapy, for cis patients. The discussion also found that LGBTQ+ New Yorkers are still paying out-of-pocket for surprise bills, even as they should be protected under New York’s Surprise Bill Law.

LGBTQ+ New Yorkers should know that they can get support from the State and from advocates if they experience discrimination in the health care system. New York State requires coverage for all gender-affirming treatment and last year required NYS-regulated insurance carriers to develop evidence-based medical necessity criteria for gender-affirming care. All plans are required to submit their criteria to the State for approval and in June the State announced that carriers are complying with the requirements. This is important because it means medical necessity decisions are more standardized and if anything goes wrong, plan members have documentation of what the plan was supposed to do. Until the State required it, many plans had no written policies on gender-affirming care. When they did, their policies didn’t always match medical best practices and categorized necessary treatments as cosmetic.

In its “Health Coverage Information for Transgender New Yorkers” guide, the state describes the process for appealing denials or filing complaints with the state when your rights have been violated. You can also get help from programs like the Community Health Advocates. They can help you no matter what type of insurance you have. Fighting to get health care you need can be exhausting and painful – if you want help, you don’t have to take on the entire burden by yourself.

CHA advocates can also help with the surprise bills that so many focus group participants described. These billing problems included bills that are clearly covered under New York’s Surprise Bill law and receiving multiple bills of varying amounts for one service. One participant received a medical bill that was so unclear she could not find contact information to pay it, even after multiple calls to the hospital where she received care. Another described conversations with their providers’ billing office as feeling “like a tennis ball being bounced around different courts.”

New York should continue to monitor insurance policies on gender-affirming care and ensure that plans who violate coverage requirements are held accountable. It should also make sure that consumer assistance programs like CHA are fully funded so that patients have support dealing with unclear and unfair medical bills.

Medicare is a life-saver for older Americans, but it does have out-of-pocket costs that can expose some patients to medical debt. A new issue brief created for HCFANY by the Medicare Rights Center explains some of the causes of medical debt for people enrolled in Medicare and describes some steps patients can take to avoid it.

Some of the causes of medical debt for people covered through Medicare are the same as for people with other types of insurance. More and more New Yorkers say they cannot afford to pay for care because of deductibles and out-of-pocket costs. This can be especially difficult for patients who are cannot afford supplemental coverage but are not low-income enough for Medicaid.

Like other patients, people with Medicare deal with medical billing errors and service denials. Patients who have had their care plan denied by insurers are then in a position where they have to ask their doctor for a different care plan; attempt to appeal, which can be overwhelming without help; or pay on their own. Finally, Medicare patients have to navigate covered versus non-covered services. Long-term care, dental care, and even ambulances can leave them on the hook for large medical bills.

Patients with Medicare coverage should review their Medicare Summary Notice to know what bills may be coming and whether any services they’ve received in the past three months were not covered. They can get help with billing questions, appealing service denials, or finding affordable care by calling the Medicare Rights Center at 800-333-4114.

New York State should also do more to protect patients from medical debt. One reason that medical errors are so common and that it is so hard for patients to know what services are covered by what providers is because the current health care system is so fragmented. A single-payer system, like the one that would be created by the New York Health Act, would eliminate the complexity that causes so much distress for patients in today’s system.

New York should also take steps to make medical billing more fair in the current system:

- Funding consumer assistance programs,

- Capping interest rates on medical debt judgments,

- Barring providers from placing liens on patients’ homes or garnishing their wages,

- Banning facility fees, and

- Making the state’s hospital financial assistance policy easier to apply for.